“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert.” –J. Robert Oppenheimer

This man, making Christmas calls from the White House, believes the world is a sphere. And he has even flown around it! So has our beautiful FLOTUS, who happens to be his wife!

Truth and common sense must be valued by us, as individuals, in order to lastingly disempower the authoritarian fake news media. This includes the perniciously smarmy science media, which never answers for its errors and lies. I believe that the media has been responsible not only for leftist pathologies like scientism, medical fascism, and radical gender ideology, but also for reactionary movements like modern flat Earth, rejection of all medicine, and Biblical geological literalism.

Just as Wheatie’s Stormwatch Monday Open Thread was created as a place for people to openly express their thoughts and opinions, so, too, is this Thank God Thursday Open Thread, where honest but civil discussion of all topics is encouraged. This thread is also to be known as Theistic Evolution Thursdays, due to the author’s expected “pontification” about his scientific, religious, and political opinions. You are welcome to pontificate back! Free speech matters!

Please label all AI-generated content as being such, unless it is patently obvious (e.g., humorous AI images). It is important that we as individuals not begin to pretend that socially derived artificial intelligence is actually our own, as this form of stealthy social information averaging and feedback would be one more pretense and deception between people, in service of stupid Marxist socialism, and of those who wish to substitute their communally protected lies for actual truth.

The source of alleged truth matters, not for the truth itself, but for validation.

And yes, it’s THURSDAY…again.

And that’s it. We’re done stealing from Wheatie.

OK – maybe her rules need to be posted.

No food fights.

No running with scissors.

If you bring snacks, bring enough for everyone.

Other rules may be derivable from these, and that conjecture is left for discussion.

If there is nothing beyond the “W” below, then this is a placeholder. For health reasons, I can’t always post a timely opinion before each Thursday, but I will try. Otherwise, you have this placeholder post, where YOU provide the content. Enjoy!

W

Thursday Trinkets – THEY’RE HERE!!!

(1) Let’s start this off right!

(2) Have you ever heard of [badly] exploding shotgun slugs? Enjoy some humorous backyard ballistics.

(3) Skip over this one if spiders creep you out. Think of worrisome American spiders as 3 categories. Black widows, brown recluses, and “other”. This is about “other”. They’re not so bad, but you might want to pay attention to them.

(4) The end of the Bronze Age is fascinating.

(5) How about an instrumental hymn? Does it sound familiar? Words are provided below!

Blessed Assurance

(Verse) Blessed assurance, Jesus is mine! O what a foretaste of glory divine! Heir of salvation, purchase of God, Born of His Spirit, washed in His blood.

(Chorus) This is my story, this is my song, Praising my Savior all the day long; This is my story, this is my song, Praising my Savior all the day long.

(Verse) Perfect submission, perfect delight, Visions of rapture now burst on my sight; Angels descending bring from above Echoes of mercy, whispers of love.

(Chorus) This is my story, this is my song, Praising my Savior all the day long; This is my story, this is my song, Praising my Savior all the day long.

(Verse) Perfect submission, all is at rest, I in my Savior am happy and blest; Watching and waiting, looking above, Filled with His goodness, lost in His love.

(Chorus) This is my story, this is my song, Praising my Savior all the day long; This is my story, this is my song, Praising my Savior all the day long.

Joe Biden never won. This is our Real President – 45, 46, 47.

AND our beautiful REALFLOTUS.

This Stormwatch Monday Open Thread remains open – VERY OPEN – a place for everybody to post whatever they feel they would like to tell the White Hats, and the rest of the MAGA/KAG/KMAG world (with KMAG being a bit of both).

Our various sister sites, listed in the Blogroll in the sidebar

Our beloved country is under Occupation by hostile forces.

Daily outrage and epic phuckery abound.

We can give in to despair…or we can be defiant and fight back in any way that we can.

Joe Biden didn’t win.

And we will keep saying Joe Biden didn’t win until we get His Fraudulency out of our White House. Which we did, but whatever. We love this picture!

Wolfie’s Wheatie’s Word of the Week:

winglet

noun

a small wing

Used in a sentence

A winglet is a small wing, often used to augment larger wings on, for example, aircraft.

Shown in a picture

Explained in a video

MUSIC!

Wings – winglets – whateverlets!

THE STUFF

This is an EXTREMELY interesting LINGUISTIC analysis of the Biblical account of Eve’s creation from Adam. Not only is the whole “rib” thing now a highly questionable translation – the “maleness” of pre-division Adam is in play.

Bottom line – the translation presented here sounds much smarter than the one that critics of the Bible love to cite. I’m still not a “literalist” on Genesis – but I think the metaphorical nature of the Genesis account just got way smarter by this translation and interpretation.

Anesthesia and surgery. Useful stuff. Even in an analogy.

This man, making Christmas calls from the White House, believes the world is a sphere. And he has even flown around it! So has our beautiful FLOTUS, who happens to be his wife!

Truth and common sense must be valued by us, as individuals, in order to lastingly disempower the authoritarian fake news media. This includes the perniciously smarmy science media, which never answers for its errors and lies. I believe that the media has been responsible not only for leftist pathologies like scientism, medical fascism, and radical gender ideology, but also for reactionary movements like modern flat Earth, rejection of all medicine, and Biblical geological literalism.

Just as Wheatie’s Stormwatch Monday Open Thread was created as a place for people to openly express their thoughts and opinions, so, too, is this Thank God Thursday Open Thread, where honest but civil discussion of all topics is encouraged. This thread is also to be known as Theistic Evolution Thursdays, due to the author’s expected “pontification” about his scientific, religious, and political opinions. You are welcome to pontificate back! Free speech matters!

Please label all AI-generated content as being such, unless it is patently obvious (e.g., humorous AI images). It is important that we as individuals not begin to pretend that socially derived artificial intelligence is actually our own, as this form of stealthy social information averaging and feedback would be one more pretense and deception between people, in service of stupid Marxist socialism, and of those who wish to substitute their communally protected lies for actual truth.

The source of alleged truth matters, not for the truth itself, but for validation.

And yes, it’s THURSDAY…again.

And that’s it. We’re done stealing from Wheatie.

OK – maybe her rules need to be posted.

No food fights.

No running with scissors.

If you bring snacks, bring enough for everyone.

Other rules may be derivable from these, and that conjecture is left for discussion.

If there is nothing beyond the “W” below, then this is a placeholder. For health reasons, I can’t always post a timely opinion before each Thursday, but I will try. Otherwise, you have this placeholder post, where YOU provide the content. Enjoy!

W

Thursday trinkets are here! Take your pick! This one is “buggy”!

(1) Ladybugs. All kinds – both the old American ones, and the imported Chinese invasive ones that try to bite to hold on but just pinch. And the LARVAE. Ewwww – larvae. AI has opinions about them. Sorry that this one has to be watched on YouTube.

Let’s finish off with the most common and closest look-alike, IMO – the Western Conifer Seed Bug (WCSB). This is America’s version of the Chinese ladybug, an invasive American species hitching a ride to the rest of the world! BUT IT’S CUTE! And it only stinks [LIKE BANANAS!] or pokes you if you manhandle it!

Their primary defense is to emit an unpleasant-smelling alarm pheromone;[2] however, if handled roughly they will stab with their proboscis, though they are hardly able to cause injury to humans as it is adapted only to suck plant sap and not, as in the assassin bugs, to inject venom.

PS – a great (and FREE) scientific article about controlling the invasive WCSB.

Joe Biden never won. This is our Real President – 45, 46, 47.

AND our beautiful REALFLOTUS.

This Stormwatch Monday Open Thread remains open – VERY OPEN – a place for everybody to post whatever they feel they would like to tell the White Hats, and the rest of the MAGA/KAG/KMAG world (with KMAG being a bit of both).

(cosmology) the original matter that (according to the big bang theory) existed before the formation of the chemical elements

Used in a sentence or two

Ylem is a term that originates from the ancient Greek word “hulē,” which translates to “matter” or “stuff.” In the context of cosmology, ylem refers to the primordial substance or state of matter that existed before the formation of the atomic elements we recognize today.

This man, making Christmas calls from the White House, believes the world is a sphere. And he has even flown around it! So has our beautiful FLOTUS, who happens to be his wife!

Truth and common sense must be valued by us, as individuals, in order to lastingly disempower the authoritarian fake news media. This includes the perniciously smarmy science media, which never answers for its errors and lies. I believe that the media has been responsible not only for leftist pathologies like scientism, medical fascism, and radical gender ideology, but also for reactionary movements like modern flat Earth, rejection of all medicine, and Biblical geological literalism.

Just as Wheatie’s Stormwatch Monday Open Thread was created as a place for people to openly express their thoughts and opinions, so, too, is this Thank God Thursday Open Thread, where honest but civil discussion of all topics is encouraged. This thread is also to be known as Theistic Evolution Thursdays, due to the author’s expected “pontification” about his scientific, religious, and political opinions. You are welcome to pontificate back! Free speech matters!

Please label all AI-generated content as being such, unless it is patently obvious (e.g., humorous AI images). It is important that we as individuals not begin to pretend that socially derived artificial intelligence is actually our own, as this form of stealthy social information averaging and feedback would be one more pretense and deception between people, in service of stupid Marxist socialism, and of those who wish to substitute their communally protected lies for actual truth.

The source of alleged truth matters, not for the truth itself, but for validation.

And yes, it’s THURSDAY…again.

And that’s it. We’re done stealing from Wheatie.

OK – maybe her rules need to be posted.

No food fights.

No running with scissors.

If you bring snacks, bring enough for everyone.

Other rules may be derivable from these, and that conjecture is left for discussion.

If there is nothing beyond the “W” below, then this is a placeholder. For health reasons, I can’t always post a timely opinion before each Thursday, but I will try. Otherwise, you have this placeholder post, where YOU provide the content. Enjoy!

W

Enjoy the first set of Thursday trinkets for March!

(1) Fake Feynman AI does a nice job here of being our Silicon Steve – explaining why [probably] Venus rotates BACKWARDS relative to the other planets of the solar system.

Watch for the typographical errors by the writing AI, which get sucked up into face-palm narration by the vocalization AI. It’s just stupid and cringe. Nevertheless, the science is good.

(2) An interesting chess rematch narrated by DrMike – check it out.

(3) Transitional hominin species Homo habilis gets a new set of skeletal remains, confirming the earlier ones, and our favorite junior anthropologist (Erika, a.k.a. Gutsick Gibbon) summarizes both the background science and the new paper on the new find. The real science can be a bit boring, but that’s often definitive for real science.

(4) Reaction video to (IMO) one of the best live rock performances from back in the mid-70s – by that band called Rush.

Yes, it’s annoying that she keeps interrupting the good parts, so here it is without interruption.

And if you’d prefer a shorter version with video, we have that, too!

(5) OK, how about more Rush, but with a SuSE twist? You may have heard this parody before, but it’s worth a listen to appreciate how well it’s re-done here.

(6) This is ….. different. An AI, heavy metal version of “The Old Rugged Cross”.

(7) You know, I think I’ll stick to the calming versions of these hymns!

Joe Biden never won. This is our Real President – 45, 46, 47.

AND our beautiful REALFLOTUS.

This Stormwatch Monday Open Thread remains open – VERY OPEN – a place for everybody to post whatever they feel they would like to tell the White Hats, and the rest of the MAGA/KAG/KMAG world (with KMAG being a bit of both).

Our various sister sites, listed in the Blogroll in the sidebar

Our beloved country is under Occupation by hostile forces.

Daily outrage and epic phuckery abound.

We can give in to despair…or we can be defiant and fight back in any way that we can.

Joe Biden didn’t win.

And we will keep saying Joe Biden didn’t win until we get His Fraudulency out of our White House.

Wolfie’s Wheatie’s Word of the Week:

mungo

noun

shoddy cloth made from shredding old or waste woven material

material of short fiber and inferior quality obtained by deviling woolen rags or the remnants of woolen goods, specifically those of felted, milled, or hard-spun woolen cloth, as distinguished from shoddy, or the deviled product of loose-textured woolen goods or worsted — a distinction often disregarded

low-quality wool

a slang term, sometimes derogatory, for a person who is rough, uncivilized, uneducated, unpleasant, perceived as inferior, etc.

one spelling of a Filipino dish made with mung beans (alternatively munggo)

additional proper names, including parks (2 kinds), people, and places

Used in a sentence

Retrosaria Mungo is a lovely worsted weight yarn made in Portugal. Mungo is made with 50% cotton which making it ideal for warmer weather knits. Mungo is entirely spun from pre-consumer waste generated by Portuguese spinning mills making it an amazing and sustainable yarn!

Shown in a picture

Shown in a video

MUSIC!

Mungo Jerry!

THE STUFF

This is a gift for Gail. It is about a Scottish explorer of Africa, by the odd name of Dr. Mungo Park. It is a brilliant bit of insight into the early days of the British Empire.

Up to my neck in “AI slop” videos about Dr. Park, I found this human-created GEM by pure accident. But it has a very different take.

There are Important Notifications from our host, Wolf Moon; the Rules of our late, good Wheatie; and, certain caveats from Yours Truly, of which readers should be aware. They are linked here. Note: Yours Truly has checked today’s post for any AI-generated content. To the best of her knowledge and belief, there is none. If readers wish to post any AI-generated content in the discussion thread for today’s post, they must cite their source. Thank you.

Do not forget to LABEL AI articles video and such.

Because of the very Pro-Israel stance of the Q-Tree I was going to stay out of this fight and had the article below this planned. However, despite the fact I am old with few years left & have no children, I do love my country and would prefer it NOT turn into a Commie-Islamic Hell hole. Unfortunately that is exactly what will happen if we lose the mid-terms.

Rich Baris of the People’s Pundit, is about the only legit pollster, I know of. He says we WILL lose the mid-terms and why. Given Tucker Carlson, Candice Owens and others I thought this alternative view should be explored. As Burning Bright says, we are in a ‘War of Stories’

We’ve been in the field every single day since before he [Trump] was sworn into office, and his approval rating hasn’t budged from its historical high.

Americans didn’t agree with everything Trump was doing in first term. They do now. It’s different..

Americans agree with what he’s doing and the Left trotting out an angry Morgan and crying Selena isn’t going to cut it this time. The Left is going to have to come up with a reformed policy platform, whether they mean it or not (almost certainly they won’t), instead of the outrageous and ignorance machine.

And less than a month later Baris says the voters mood has changed and we will lose the mid-terms. What happen in that month?

POTUS sent American military to the middle east and is now threatening Iran.

At 17 minutes Baris says what people here are NOT going to like hear. Remember this guy is polling people every day and he is telling us what Americans think.

The Israel First attitude in the senate is what is going to lose us the Midterms. Just like ‘RACIST’ is used to shout people down, Anti-semite is used to silence people. They may go silent BUT THAT JUST BUILDS RESENTMENT.

He says 30% of the republicans in SC will not vote for Miss Lindsey because of this.

PARTIAL TRANSCRIPT

This is something very dark we are not allowed to talk about because every time you do someone calls you an antisemite. Mark Levin because of my polling [called me an antisemite] and said it is in my DNA because I am European… It [being called antisemite] scares people and they no longer want to talk about it and they [the Israel first crowd] are free to do what they are doing, go to the White House… Netanyahu has been there more than any body and there is a reason for it. The Ted Cruz & Lindsey Grahams & Bebe Netanyahu’s view the Trump presidency as the last chance to do what Israel has long wanted to do. That is why you heard Mike Huckabee as the US Ambassador say during the Tucker interview “It would not bother me if they took it all.”Because there is a very real agenda. They are already talking about Turkey next year. They want to take parts of Turkey. I kid you not. This is Nuts. They [the Israel lobby] put themselves ahead of you. It does not matter if you are pro-Israel or not. This is what happened. They put THEIR INTERESTS ahead of you.

Israeli Finance Minister Bezalel Smotrich announced plans to promote Palestinian emigration, annul the Oslo Accords, annex the West Bank, and extend Jewish settlements as part of the next government’s agenda.

….He [Smotrich] linked the coming political phase in Israel to the remaining term of US President Donald Trump, who began a four-year term in January 2025, calling it a “window of opportunity” to enact sea changes, including “dismantling the Palestinian Authority and disarming the West Bank.”

BACK TO TRANSCRIPT

19:30– They knew full well last year, with the bombing of Iran, it would have taken Trump’s peak presidency. By that I mean a certain amount of time during the first year when Congress will do big things. Because once we go into the second year, which I tried to warn people about, Congress will not do big things. The do not want to cast controversial votes. They do not want to take unnecessary risks during an election year. The donors are breathing down their backs.You really have 8 months and THAT’S IT. That is what you have got as a president to get your agenda through.

They [Israel Lobby] decided to hijack the last of that eight months because they figured their interests were more important than the American public’s. They don’t give a damn about you.

They figure the next time is a Democrat president and we will get nothing from them. So we have to get as much as we can from Donald Trump. AND THEY DID GUYS AND THEY WON. I hate to say this but that is the reality in Washington DC. A president’s agenda is a constant tug of war between the blob [Mike Benz’ term for the Cartel — GC] and the Donor Class and what the American people wants...

20:20 — You can not have 60% of the country since the bombing of Iran the first time last year, tell the president we are over this crap and get back to domestic policy. Then have him ignore it. Then Trump MOCKS PEOPLE with the make Iran great again posts on social media.

He did exactly what Rush Limbaugh in his final days warned him not to do… He broke the bond between him and the American People….

Benjamin Netanyahu returned to Israel after a closed-door meeting with President Donald Trump in Washington

Comment byGhostofBasedPatrickHenry:Like everyone I follow at Badlands, Ghost is a Christian. However he is not particularly fond of Israel. He is also well read historically, and IIRC has been to the middle east. He can lay out logically the point of view of Christians who want nothing to do with more war in the middle east.

Also I noticed someone yanked out the tired old “Iran’s a week away from having a nuclear bomb” Remember The Gulf of Tonkin Incident that served as a catalyst for U.S. involvement in the Vietnam War? An incident that NEVER HAPPENED?

…There is always the possibility that a kinetic attack is imminent. If that’s what is in the cards, then President Trump certainly wouldn’t telegraph such plans or intent to the world beforehand.

But I have long asserted, and continue to maintain, that such calculus does not lead us to the Golden Age. The cycle of violence has to be broken, and Iran represents one of the longest-running pledges for large scale violence of my lifetime.

It has never been a question of ‘if’ we will have a war with Iran; it has always been a question of ‘when.’

Our beloved elites, of course, could never fully explain why such an idea would be in any way appealing to the American People. Why should we go give more of our families’ blood and treasure to fight an enemy on the other side of the world that poses no clear and present danger to America? (Spare me all of Mark Levin’s talking points. That’s all a bunch of NeoCon bullshit.)

They want us to believe that Israel doesn’t control our government. They say that I am an antisemite for suggesting such a thing. And yet, things like this keep happening that support—if not affirm—the allegation.

Can somebody explain to me why Iran needs a new government? Even if we were to assume that the people running that place were the worst tyrants who ever lived, in terms of how the government treats Iranians, why exactly is that our problem? Despite all the consternation and hyperventilating from the kosher crowd (Loomer, Levin, Lady Lindsey) there is no evidence to suggest Iran poses a threat to the United States or even to Israel.

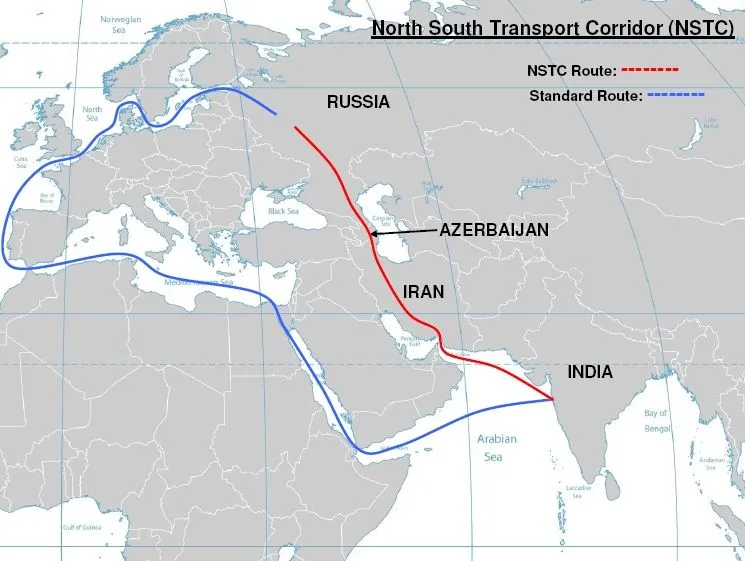

Not to mention that Iran, which was once geopolitically isolated, now has strong international relations with a number of world powers, most notably Russia and China. Iran has also become a geographic centerpiece of the North-South Transport Corridor, which is a trade route developed by the Shanghai Cooperation Organization to compete with the Suez Canal.

The deep economic entanglement between these nations will actually keep Iran accountable as economic pressure from both inside and outside of the country will promote peace and deter kinetic conflict.

Put simply, there is absolutely no reason to believe that Iran wants to start a war with Israel or the US—even assuming that Iran harbors ill-will toward Israel and would prefer to see it somehow destroyed. The point is that Iran is not going to start or provoke such a war with Israel because it knows that it will end up fighting the US and Europe.

So why the hell are we allowing the Israel lobby to drag us into this situation?

Ghost does not say, but I will, If the USA attacks Iran on Israel’s behalf, it could be the beginning of WWIII given Iran’s entanglement with China and Russia. Of course nothing would please the Cabal more, than to plunge the USA & the world into another major war.

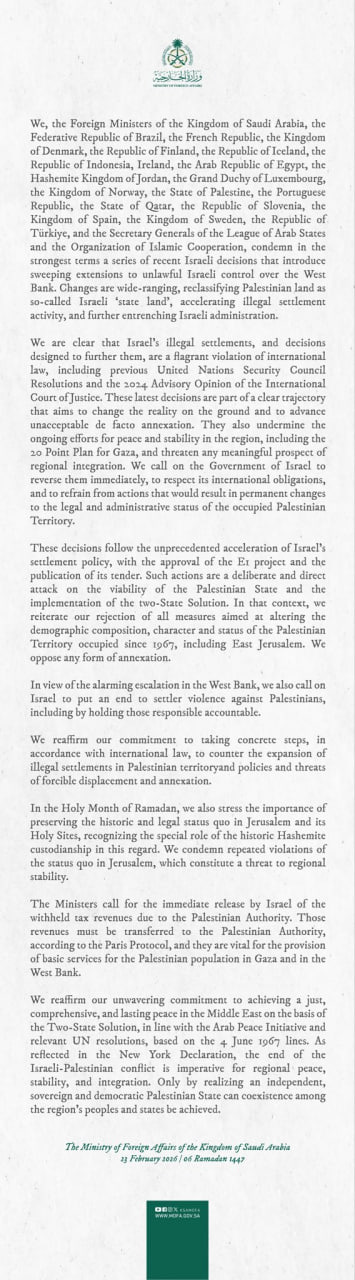

Here is a lengthy formal statement posted by the Kingdom of Saudi Arabia:

These are the countries signing this document:

We the Foreign Ministers of the Kingdom of Saudi Arabia, the Federative Republic of Brazil, the French Republic, the Kingdom of Denmark, the Republic of Finland, the Republic of Iceland, Ireland, the Republic of Indonesia, the Arab Republic of Egypt, the Hashemite Kingdom of Jordan, the Grand Duchy of Luxembourg, the Kingdom of Norway, the State of Palestine, the Portuguese Republic, the State of Qatar, the Republic of Slovenia, the Kingdom of Spain, the Kingdom of Sweden, the Republic of Turkiye

Continued from Ghost.

Allow me to demonstrate how disrespectful these Israelis are toward President Trump. Explain to me how this public statementfrom Israeli Finance Minister Bezalel Smotrich is not undermining Trump’s efforts for peace?

How about Ze’ev Elkin from the Finance Ministry yesterday asserting that Israel will not financially contribute to Trump’s Board of Peace? Is that disrespectful?

What about last month when all of the top officials in Netanyahu’s government—including Smotrich—formally rejected President Trump’s Board of Peace? Is that disrespectful?

Meanwhile, here is the opposition leader to Netanyahu’s government, Yair Lapid, declaring that he will stand with Bibi in a war against Iran. Because even this former news anchor turned “center-left” progressive politician wants a war with Iran, and is willing to give Bibi all the support he needs to carry it out. Lapid even went on (in Hebrew) to express empathy for the Greater Israel that Mike Huckabee conceptualized in his interview with Tucker.

And just as I thought, it looks like POTUS Trump may be pulling a peaceful rabbit out of his red ball cap despite the Israelis lust for more territory and war.

Iran’s Deputy Foreign Minister Majid Takht-Ravanchi said Tuesday Tehran is ready to swiftly reach a nuclear deal with Washington, stressing negotiations in Geneva will focus solely on the nuclear issue and urging diplomacy to avoid regional conflict.

Now we need Ukraine to give up and actually come to the table before the midterms.

Four Horsemen, Eight Families & Their Global Intelligence, Narcotics & Terror Network

Excerpts from The Third World Traveler

p5

Kermit Roosevelt, the Mossadegh coup-master [Iran, 1953] admitted in his memoirs that SAVAK was 100% created by the CIA and Mossad, the Israeli intelligence agency that acts as appendage of the CIA.

p7

No corporations profited more than US defense contractors [from the 1953 Iran coup]. From 1950-63 the Middle East received 3% of US military aid to the world. From 1971-75 it received 60.2%. [21] The bulk of it went to Israel, Saudi Arabia and Iran. Iran and Saudi Arabia were the “Twin Pillars” in President Nixon’s 1972 Guam Doctrine. Nixon and his cronies saw these two nations as critical to ensuring a steady cheap supply of crude oil to the US. Saudi reserves are estimated at 261 billion barrels, while Iran sits atop nearly 100 billion barrels.

… Revenues received by both the Shah and his House of Saud counterparts were recycled back into US money-center banks JP Morgan, Chase Manhattan and Citibank. These banks own huge blocks of stock in the Four Horsemen [Big Four oil companies – Royal Dutch Shell, ChevronTexico, ExxonMobil, British Petroleum] and in the defense contractors which now jostled for position in both Tehran and Riyadh. Chase Manhattan owned Iran’s Central Bank – Bank Markazi. The international bankers were the main beneficiaries of this new oil for arms quid pro quo. In Iran the Shah was given carte blanche on US arms purchases. Iran came to account for 25% of US military sales.

p10

The State Department once called the Middle East, “a stupendous source of strategic power and one of the greatest material prizes in world history, the richest prize in the world in the field of foreign investment.”

p10

Oil revenues financed the Shah’s military procurement program. He agreed to recycle surplus petrodollars into US banks, mainly Chase Manhattan, which his good friend David Rockefeller chaired. Iran’s Central Bank, the Bank Markazi, acted as wholly-owned subsidiary of Chase Manhattan. Oil revenue also went to banks like BCCI where it funded CIA covert operations

p11

The Shah served as cop on the beat for the US in the Persian Gulf, while Israel filled that role in the Mediterranean. President Truman called Israel, “a stationary aircraft carrier to protect US interests in the Mediterranean and the Middle East”.

p15

Within a few years of the Iranian Revolution, the CIA was helping Ayatollah Khomeini identify nationalist leaders so he could target leftists who had formed the Committee of 60, which led the Iranian revolution. In 1983 the CIA and British MI6 supplied a long list of Tudeh Party members to Khomeini. The Ayatollah unleashed a reign of terror against the left; assassinating, torturing and imprisoning over 10,000 Tudeh members and supporters. In 1989 many of those imprisoned were sentenced to death.

p16

SAVAK used heroin money to finance counter-revolution in Iran. The CIA allowed wealthy Iranians to smuggle their heroin into the US using diplomatic pouches. Iranian revolutionaries cracked down on the heroin trade, which had thrived under the Shah.

p17

Zbigniew Bzrezinski co-founded the Trilateral Commission (TC) in 1973 with David Rockefeller… The stated purpose of TC was to form a triad of global influence consisting of North America, Western Europe and Japan.

The TC published The Crisis of Democracy in 1975. One of its authors, Harvard professor Samuel P. Huntington, is a prominent writer for the CFR publication Foreign Affairs. Huntington, intellectual darling of the global elite, argued that America needed “a greater degree of moderation in democracy”.

The TC paper suggested that leaders with “expertise, seniority, experience and “special talents” were needed to “override the claims of democracy”. More recently Huntington has been pushing his “Clash of Civilizations” thesis, which argues that war between the West and Islamic nations is inevitable.

This part segues into the next about South America, drugs & banks.

p111 BCCI [Bank of Credit and Commerce International] would become the mixing bowl into which Persian Gulf petrodollars were stirred with generous helpings of drug money to finance worldwide covert operations for the CIA and its Israeli Mossad and British MI6 partners.

BCCI was the bank of choice for the world’s most notorious dictators, including the Somoza family, Saddam Hussein, Philippine strongman Ferdinand Marcos and Haiti’s Jean-Claude “Papa Doc” Duvalier. The South African apartheid regime used BCCI, as did Manuel Noriega.

… With branches in 76 countries, BCCI dealt in conventional and nuclear weapons, gold, drugs, mercenary armies, intelligence and counterintelligence… The bank had close relations with the CIA,Pakistan’s ISI intelligence service, the Israeli Mossad and Saudiintelligence agencies… BCCI’s main stockholders were monarchs and wealthy oil sheiks from the GCC [Gulf Cooperation Council] nations.

… BCCI was founded 1972 in Pakistan by Agha Hasan Abedi, a close friend of Pakistani military dictator Zia ul-Huq… BCCI took its wings when Bank of America put up $2.5 million for a 30% stake in BCCI. At that time Bank of America was the largest bank in the world, controlled by N.M. Rothschild & Sons.

U.S. President Donald Trump hosted Colombian President Gustavo Petro for their first in-person meeting at the White House on February 3, lasting over two hours in a private Oval Office session.

The encounter, attended by top officials including Vice President JD Vance, Secretary of State Marco Rubio, and U.S. Senator Bernie Moreno on the American side, and Foreign Minister Rosa Villavicencio, Defense Minister Pedro Sánchez, and Ambassador Daniel García-Peña on the Colombian side, produced unexpectedly positive tones and visuals after a year of public tensions, threats, and insults between the two leaders.

Trump described the meeting positively, stating “We got along very well” and noting prior unfamiliarity despite past friction.

Petro called himself “optimistic and positive,” reporting discussions on “concrete problems and joint pathways,” and left with a modified MAGA hat reading “Make Americas Great Again.”

Trump gifted Petro a signed copy of “The Art of the Deal” inscribed with “You are great” and “I love Colombia,” which Petro shared on X.

Discussions focused on counternarcotics cooperation...

Present given to POTUS Trump by President Gustavo Petro

…While we don’t have any hard facts yet on what specifically was achieved during the meeting, both Trump and Petro have independently said in interviews they agreed to collaboration on operations against the cartels, as well as Trump looking into lifting the sanctions he recently imposed on Petro and his family.

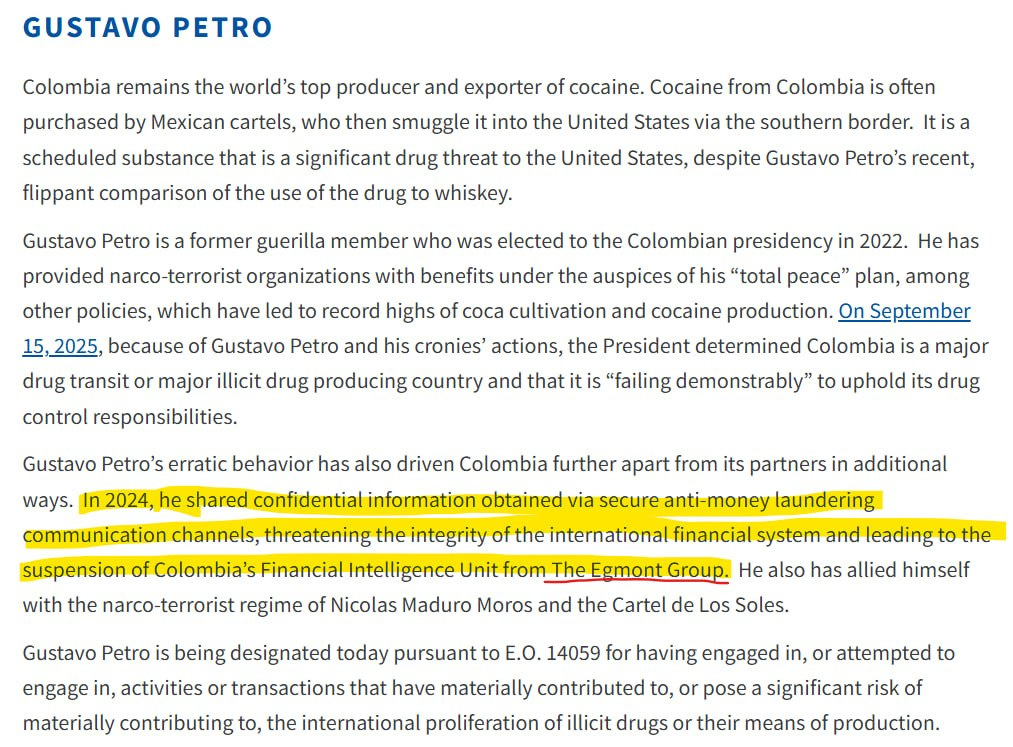

I went and read the document from the Treasury that imposed the sanctions on Petro, and found a paragraph that stuck out to me.

So what is this organization? I asked ChatGPT.

So the Deep State literally has an international intelligence unit that tracks all the financial crime information that is shared between governments, and when Gustavo Petro—the one world leader that we know for certain is going after the cartels—shared privileged information about the group that he had obtained through official channels, it compromised the integrity of the organization and led to the suspension of Colombia from the team.

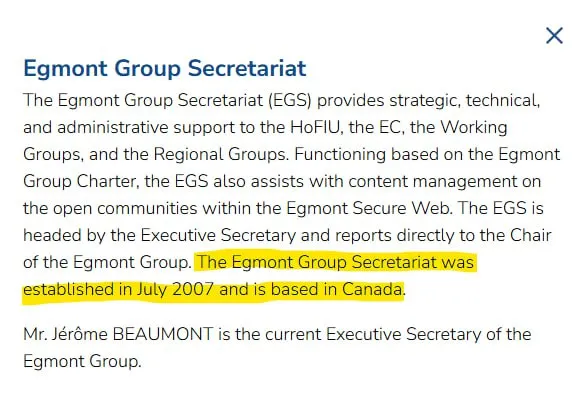

So where is this organization located? Where is their headquarters?

CANADA??? You have got to be kidding me! And this group tracks bank transactions and passes suspicious activity on to the FBI and DOJ.

The Mark Carney lore as the king of all central bankers has now significantly increased.

Canada may very well be the final boss.

Sidenote: I may do a stream this afternoon to dig into all of this. Stay tuned.

It is worth noting that after his meeting with President Trump, Petro held a press conference where he said that the next step in fighting the cartels is to target the major financiers and international structures that operate outside of Colombia.

Colombian President Gustavo Petro announced that he had evaded an assassination attempt when intelligence revealed a plot to fire on his helicopter, forcing an abrupt route change. During a government meeting broadcast live on the presidential administration’s YouTube channel, Petro stated that he had “avoided being killed” and described how the aircraft—carrying him along with his children—was rerouted to fly for four hours over the open sea before landing at an unplanned location.

The report, originating from Buenos Aires and published by TASS on February 10, 2026, provided no additional details on the alleged perpetrators, investigation status, or specific threats involved.

Petro met with President Donald Trump on February 3, 2026 and an assassination attempt happens on February 10. On February 11, 2026, the FAA abruptly closed airspace around El Paso, Texas, due to drone activity near the U.S.-Mexico border. An assassination attempt against POTUS Trump happens on February 22, 2026. Nemesio Rubén Oseguera Cervantes, known as “El Mencho” is also killed on February 22, 2026. Sure was a busy couple of weeks!

“I didn’t land where I was supposed to because there were fears that the helicopter, in which my children were also located, would be fired upon,” he said at a government meeting broadcast on the presidential administration’s YouTube channel.

According to Petro, he “avoided being killed.” “We flew for four hours over the open sea and arrived where we didn’t plan to,” he said.

Our guy, Petro, has been on a heater lately.

Just last week, after meeting with President Trump at the White House, he held a press conference where he announced that he had proposed to Trump an international joint operation to go after the most powerful cartel bosses at the very top of organized crime— bankers, financiers, corporate executives, etc.

Then they tried to assassinate him.

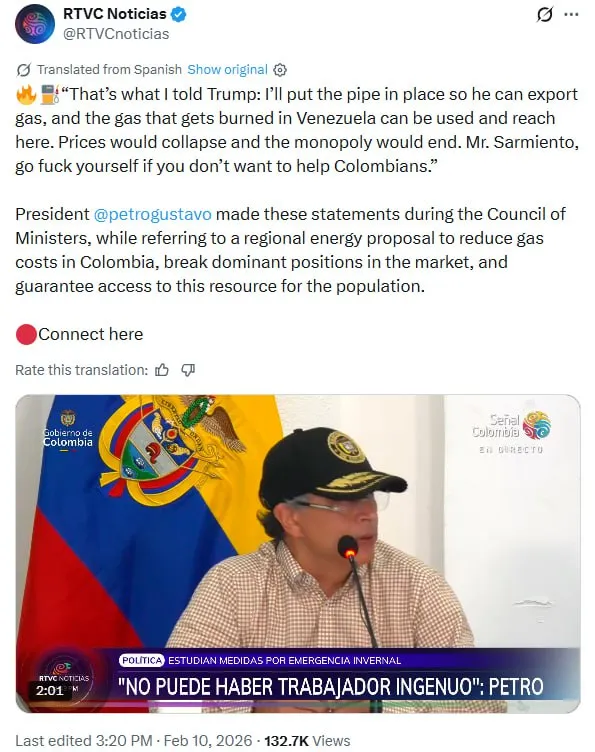

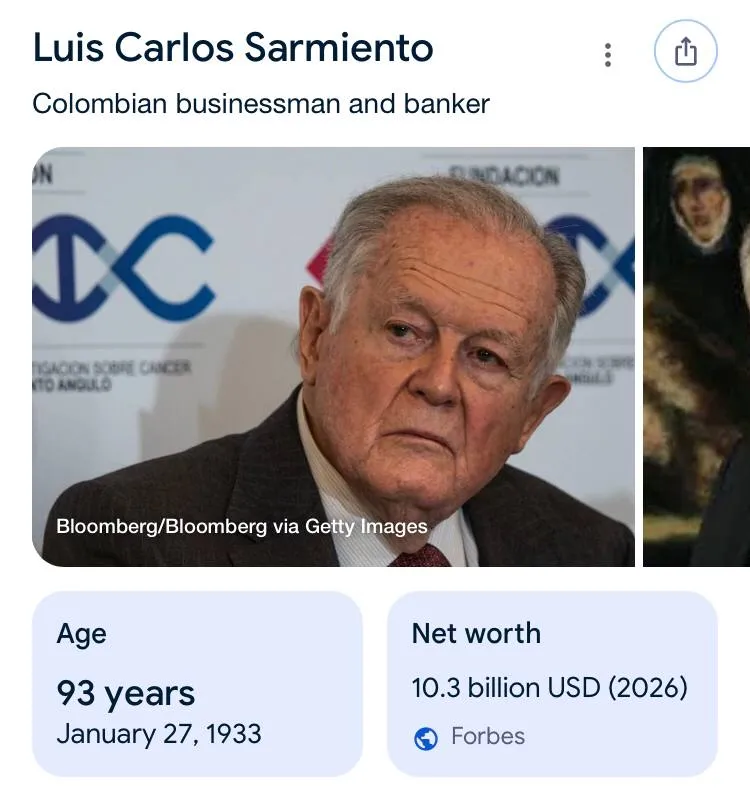

At this same press conference where he disclosed the assassination attempt, he also called out a Colombian billionaire banker named Luis Carlos Sarmiento, telling him that he can “go F yourself” if he was going to stand in the way of a pipeline project with Venezuela that Petro had discussed with Trump.

Sarmiento is worth roughly $10 billion. [Note he is also a banker -GC]

No wonder they want to kill this guy. He is just about the most flippantly defiant world leader since… well, since Nicolas Maduro.

Assuming this assassination attempt story is real, who could blame Petro for having this attitude?…

The Trump Administration confirmed that “cartel drones” entered US airspace near El Paso, Texas, and were disabled by the FAA and the Department of War. Secretary Duffy (Transportation) posted on X:

“The FAA and DOW acted swiftly to address a cartel drone incursion. The threat has been neutralized, and there is no danger to commercial travel in the region. The restrictions have been lifted and normal flights are resuming.”

The FAA earlier issued a surprise notice shutting down the airspace above El Paso, a major city in west Texas on the US-Mexico border, and halting all flights up to 18,000 feet for 10 days due to “special security reasons.” The restricted area covered a 10-mile radius, and restrictions were lifted Wednesday night.

Business Insidercites anonymous officials claiming that the administration disabled the drones using counter-drone measures. The department did not publicly specify the exact technology used.

Mexican President Claudia Sheinbaum rejected reports of the alleged drone incursion, stating, “There is no information about the use of drones on the border,” according to reporting by Newsweek. The same article reports that Representative Tony Gonzales responded to the drone news:

“For those of us who live and work along the border, daily drone incursions by criminal organizations are part of everyday life. It’s a Wednesday for us.”

All the Fake News that Brave pulled up on its first page say it was just party balloons.

So Colombian President Gustavo Petro comes to town last week (nearly gets assassinated later on the way home to Colombia) and vows that he and Trump are working together to bring down cartels and the bankers that finance them.

Our friend, Eric Rice, presented an interesting question: Who sold Mexico the drones?

This is an interesting question, and I found an interesting article from 2015.

…First the FFA shuts down the airspace around El Paso. Then we get conflicting reports about an invasion. This is definitely an invasion.

It does seem like Mexico is the last bastion of these Hispanic narcotics cartels, and Trump has dropped plenty of signal that he considers the Mexican government in bed with cartels and therefore a threat….

For months now, I’ve been saying that Colombian President Gustavo Petro is the righteous actor—as he has spent the past three years going after the cartels.

Here is video that Petro posted to X yesterday recapping some of their operations.

Fueron a decir arrodillados que el presidente de Colombia era un narcotraficante, y que así otra guerra en Colombia.

They went kneeling to say that the president of Colombia was a drug trafficker, and that this would cause another war in Colombia. They always do the same thing. Look at reality.

This program that Secretary of the Treasury Scott Bessent is rolling out with FINcen seems to streamline the bounty system while focusing on the critical evidence: the money.

“Follow the money” is a notorious refrain not only in the Q Research community, but in the entire cultural ethos of “criminology” as well. Whether you are talking about a crime drama presented as a work of fiction on Netflix, or academic detective work, forensic accounting is the ideal method of mapping out criminal networks because the money flow is objective and traceable.

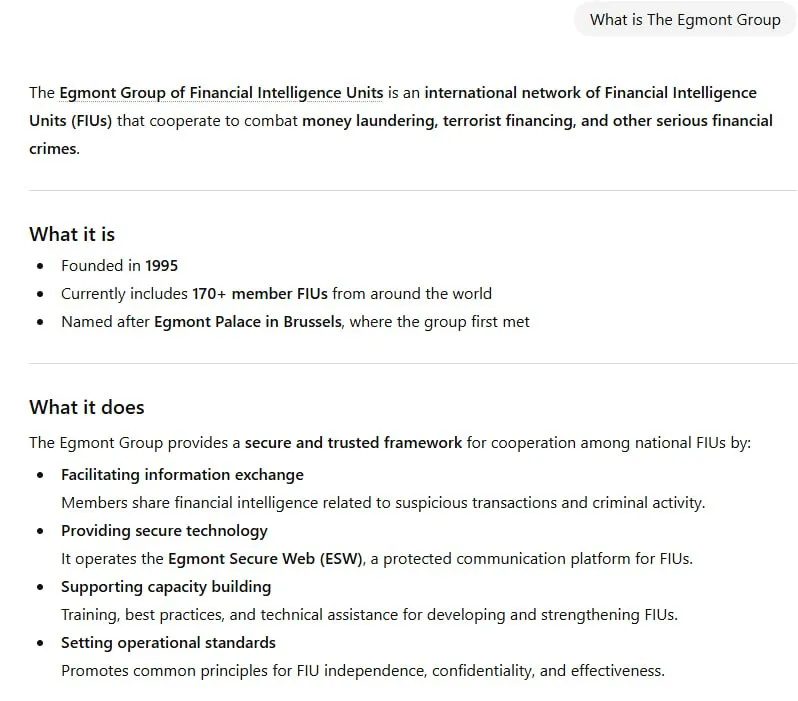

If you’ve listened to the past few episodes of Breaking History, we have been discussing FINcen and the Egmont Group. While FINcen is the financial crimes intelligence unit in the US government, the Egmonth Group is an international network of over 170 of this type of intelligence unit from nearly every government on earth. The purpose being to share in this intelligence.

Colombian President Gustavo Petro was sanctioned by the Treasury Department last year, and in the sanctioning document Petro is accused of getting Colombia’s financial crimes intelligence unit suspended from Egmont for allegedly sharing information he collected from the Egmont servers.

It is fascinating that both Petro and Maduro have accused all of the most powerful banks in the US and Europe of literally being the cartels. Petro says that it is institutions like Egmont Group that allow the criminality to continue and prosper, because it covers for them.

Bessent’s strategy is brilliant because it creates a practical incentive structure and has a reliable source of reward money. It also inherently targets the core culprit in all organized crime syndicates: the financial institutions.

We are going to pay criminals to rat out their friends. We are going to pay bureaucrats and accountants to blow the whistle on shady stuff they see around the office. And we are going to pay them with the money collected from fines imposed on the guilty parties. The idea being that the investigations will lead to criminal referrals and indictments.

Scott Bessent is weaponizing the financial system against itself by tapping into base human instincts.

We’ve been speculating for months that Mexico would be the real target for a military operation. Here’s President Trump weeks ago explaining that the cartels control Mexico.

[Video]

Yesterday, President Trump affirmed that he did offer to send in US troops to fight the cartels, but was turned down by Mexican President Claudia Sheinbaum.

[Video]

This tracks, if the cartels do actually control Mexico.

However, two weeks ago it was reported that a Mexican Senate commission approved a proposal for SEAL Team 2 to go there and train Mexican special forces to fight the cartels.

Last week, Sheinbaum formally invited the SEALs—though this was only in a training capacity.

With all of this said, it is notable that the New York Post reported that over 100 cartel bosses—including El Mencho’s brother—were quietly handed over to the Trump administration prior to the Jalisco raid where El Mencho was killed.

It could be that things are not what they seem. It could be kayfabe to keep the cartels guessing. We should continue to withhold belief (h/t: Chris Paul ) until we have enough data to adopt an informed opinion.

Personally, I do think this particular war against the cartels is real, andI think much of the cartels’ infrastructure has already been severely hampered by the efforts of Colombian President Gustavo Petro and Venezuelan President Nicolas Maduro, along with Bukele of El Salvador, among others.

As Petro is calling for Trump to lead a crusade against the bankers and financiers that support the cartels, the [Mexican] military is going after them in Mexico.

H/T patfrederick said NebraskaFilly said Rodney posted this Tweet last night:

▪️THE SUPPLIER IS DEAD.

THE CLIENT LIST SURVIVED.

When Mexican Special Forces took out El Mencho, they didn’t just find guns and drugs. They found a laptop.

On it: a single encrypted file named “CLIENTES.”

Inside: 211 names. The elite clients who ordered children and organs…

THE SUPPLIER IS DEAD. THE CLIENT LIST SURVIVED. When Mexican Special Forces took out El Mencho, they didn’t just find guns and drugs. They found a laptop. On it: a single encrypted file named “CLIENTES.” Inside: 211 names. The elite clients who ordered children and organs from “The Supplier.” Hollywood actors. Tech billionaires. Wall Street executives. And 17 sitting members of Congress. For 48 hours, the Deep State tried to bury it. The CIA tried to claim jurisdiction. The FBI tried to seize the laptop. They failed. Trump’s people got to it first. The file is now in the hands of the same military intelligence unit that is preparing for the State of the Union address. This is the kill shot. The Epstein files were the blackmail network. The Client List is the customer base. Arrests are not coming. They have already begun. Pay attention to who disappears this week. This is not politics. This is war. And the snakes can’t hide anymore.

I hope this proves true because if so it will prove more important than the Epstein Files. 48 hr rule applies of course. So far I can find nothing.

>>>>>>>>>>>>>>>>>>>>>>>>>

We don’t know what the next epoch will bring, whether or not it will be fortuitous for the American People. There is an excitement that is fueled by that uncertainty, but also burdens us with the anxiety that shrouds every future unknown. We end up choosing the devil that we know rather than charging into the darkness of that unknown. For too long, we were convinced that this anxiety was reason enough to never seek an end to this status quo, even as that status quo was quietly subverted and secretly altered in order to exploit the American People.

One day, after years of healing, perhaps the American People will have the courage, strength, and fortitude to stop these machinations dead in their tracks. Sometimes I wonder whether we were too broken psychologically to have actually saved ourselves, or whether we were lucky enough to be blessed by angels weaving divine providence. — GHOST

NOTE: Gail Combs is having very terrible back pains tonight, and WordPiss is acting up, so we have switched Wednesday and Thursday nights. Please pray for Gail’s recovery and healing!

This man, making Christmas calls from the White House, believes the world is a sphere. And he has even flown around it! So has our beautiful FLOTUS, who happens to be his wife!

Truth and common sense must be valued by us, as individuals, in order to lastingly disempower the authoritarian fake news media. This includes the perniciously smarmy science media, which never answers for its errors and lies. I believe that the media has been responsible not only for leftist pathologies like scientism, medical fascism, and radical gender ideology, but also for reactionary movements like modern flat Earth, rejection of all medicine, and Biblical geological literalism.

Just as Wheatie’s Stormwatch Monday Open Thread was created as a place for people to openly express their thoughts and opinions, so, too, is this Thank God Thursday Open Thread, where honest but civil discussion of all topics is encouraged. This thread is also to be known as Theistic Evolution Thursdays, due to the author’s expected “pontification” about his scientific, religious, and political opinions. You are welcome to pontificate back! Free speech matters!

Please label all AI-generated content as being such, unless it is patently obvious (e.g., humorous AI images). It is important that we as individuals not begin to pretend that socially derived artificial intelligence is actually our own, as this form of stealthy social information averaging and feedback would be one more pretense and deception between people, in service of stupid Marxist socialism, and of those who wish to substitute their communally protected lies for actual truth.

The source of alleged truth matters, not for the truth itself, but for validation.

And yes, it’s THURSDAY…again.

And that’s it. We’re done stealing from Wheatie.

OK – maybe her rules need to be posted.

No food fights.

No running with scissors.

If you bring snacks, bring enough for everyone.

Other rules may be derivable from these, and that conjecture is left for discussion.

If there is nothing beyond the “W” below, then this is a placeholder. For health reasons, I can’t always post a timely opinion before each Thursday, but I will try. Otherwise, you have this placeholder post, where YOU provide the content. Enjoy!

W

Here we go again! More Thursday THRILLS!

(1) Before Amelia The Goth, there was Amelia Earhart. So what happened to her? Here’s one theory with a lot of evidence, but still…..

(2) America has an ace in the “critical minerals” game. What is it? WATCH.

(3) Fire ants. NASTY. Using flies to kill them? Also NASTY, bit seemingly necessary. DETAILS.

Joe Biden never won. This is our Real President – 45, 46, 47.

AND our beautiful REALFLOTUS.

This Stormwatch Monday Open Thread remains open – VERY OPEN – a place for everybody to post whatever they feel they would like to tell the White Hats, and the rest of the MAGA/KAG/KMAG world (with KMAG being a bit of both).

This man, making Christmas calls from the White House, believes the world is a sphere. And he has even flown around it! So has our beautiful FLOTUS, who happens to be his wife!

Truth and common sense must be valued by us, as individuals, in order to lastingly disempower the authoritarian fake news media. This includes the perniciously smarmy science media, which never answers for its errors and lies. I believe that the media has been responsible not only for leftist pathologies like scientism, medical fascism, and radical gender ideology, but also for reactionary movements like modern flat Earth, rejection of all medicine, and Biblical geological literalism.

Just as Wheatie’s Stormwatch Monday Open Thread was created as a place for people to openly express their thoughts and opinions, so, too, is this Thank God Thursday Open Thread, where honest but civil discussion of all topics is encouraged. This thread is also to be known as Theistic Evolution Thursdays, due to the author’s expected “pontification” about his scientific, religious, and political opinions. You are welcome to pontificate back! Free speech matters!

Please label all AI-generated content as being such, unless it is patently obvious (e.g., humorous AI images). It is important that we as individuals not begin to pretend that socially derived artificial intelligence is actually our own, as this form of stealthy social information averaging and feedback would be one more pretense and deception between people, in service of stupid Marxist socialism, and of those who wish to substitute their communally protected lies for actual truth.

The source of alleged truth matters, not for the truth itself, but for validation.

And yes, it’s THURSDAY…again.

And that’s it. We’re done stealing from Wheatie.

OK – maybe her rules need to be posted.

No food fights.

No running with scissors.

If you bring snacks, bring enough for everyone.

Other rules may be derivable from these, and that conjecture is left for discussion.

If there is nothing beyond the “W” below, then this is a placeholder. For health reasons, I can’t always post a timely opinion before each Thursday, but I will try. Otherwise, you have this placeholder post, where YOU provide the content. Enjoy!

W

Another assortment of digital trinkets for your fascination and amazement!

(1) I know I’ve showed you this one before, but I always enjoy it. Love the intro, too. Replay!

(2) Language. Humans do it. Crows do it. Well, other primates do it, too. Another anthropology trinket.

(3) Assault machine guns are getting updated. Check out the latest improvements!

(4) Three very fast chess games, with a lot of analysis of every move. CHESS LEARING CENTER! And y’all are LEARING from the very best!

(5) MOAR Christian praise from my favorite digital hymnsmiths!

That’s all for now – as I am CLEARING the tags of LEARING. So to speak. LOL!