I AM NOT GOING TO MAKE THIS FANCY. I JUST WANT A PLACE WE CAN PUT ALL THE INFORMATION.

CORBETT REPORT: talks of Bank of England implementing Central Bank Currency and a questionaire designed to show buy in.

WHAT IS THE DELPHI TECHNIQUE? – QUESTIONS FOR CORBETT

Peter writes in to ask how we should respond to the Bank of England’s rigged survey about CBDCs. James answers by describing the Delphi method and how to anti-Delphi in real life.

https://www.bitchute.com/video/cCQeKybJhJq8/

FROM COMMENTS ON MAY 12TH

DO NOT FORGET KLAUS SCHWAB’S THREAT ABOUT CYBER ATTACKS….

The WEF “Cyber Attack” Scenario: Another Crisis “Much Worse than Covid”, Paralysis of Power Supply, Communications, Transportation

WEF: “There will be another crisis. It will be more significant. It will be faster than what we’ve seen with COVID”

TradeBait2(@tradebait2)

Offline

Coyote

Reply to Gail Combs

March 12, 2023 15:39

OK, OK. I get it.

There is no doubt they want us in the digital economy. There is no doubt half the population will never do it without a dictator forcing it. So they are setting up China to be their dictator by killing manufacturing and selling off as many of our strengths as possible. These things we know.

SVB was a creation of the cabal in the 1980s. Its primary purpose of late was to fuel the green economy, venture capital into Silicon Valley tech/research/etc., big Pharm, and other globalist type endeavors. They were the go-to for those industries and it was totally incestuous.

As for today –

First, their investment portfolio is upside down. They have $21 B of treasuries yielding 1.79% when the most recent treasury 10 year issues were at 3.9%. Enter Coothie and others with their “mark to market” accounting discussions. Add in they need to sell some of those assets due to the run. In summary, they take a big hit there.

They had too much liquidity. The Fed has been raising rates, reducing business activity. Less borrowings to earn interest, more payout of interest for higher interest rate deposits that are locked in for at least a year.

Overall economic downturn depressed access to capital for their major customers, which by nature are hard to finance conventional methods. Many would qualify for junk bond status. So those companies, who are depositors in SVB, begin drawing down deposit balances to fund their operations. This adds to SVB’s cash drain.

SVB tries to go to the markets and issue over $2 B in stock to mitigate the damage. That sparks alarm, adds to the run. Buh bye SVB.

Long term –

The major banks, many larger than SVB, are derivative monsters. That exposes them to huge risk in world currency markets as well as interest rate movements if an alternative develops that changes America from being a historical safe harbor for investment and cash. In essence, we have been using our perceived military and economic power to bend over other countries around the world to fuel our spending problem. What happens when there is a more stable alternative? i and others contend that alternative is BRICS with their gold and precious metals standard and mutually accepted currency valuation methods.

If this proceeds as it appears, our larger banks will be in major trouble. The Fed will print more money that we have ever seen. Inflation will explode. Real estate values will tank with a huge rise in defaults. Etc. That will provide the entry the globalists want to force digital currency on a scared population. It will be sold as the patriotic thing to do.

All sponsored by WEF and others in conjunction with BRICS.

Precipice.

𝗟𝗢𝗢𝗞 𝗮𝘁 𝘁𝗵𝗲 𝘀𝗶𝘁𝘂𝗮𝘁𝗶𝗼𝗻 𝗳𝗿𝗼𝗺 𝘁𝗵𝗲 𝗔𝗖𝗧𝗨𝗔𝗟 𝗚𝗢𝗔𝗟 𝗼𝗳 𝘁𝗵𝗲 𝗖𝗔𝗕𝗔𝗟. 𝗧𝗵𝗲𝘆 𝘄𝗮𝗻𝘁 𝗮 𝗱𝗶𝗴𝗶𝘁𝗮𝗹 𝗰𝘂𝗿𝗿𝗲𝗻𝗰𝘆 𝘁𝗶𝗲𝗱 𝘁𝗼 𝗮 𝘀𝗼𝗰𝗶𝗮𝗹 𝗰𝗿𝗲𝗱𝗶𝘁 𝘀𝘆𝘀𝘁𝗲𝗺 𝘀𝘂𝗰𝗵 𝗮𝘀 𝗖𝗵𝗶𝗻𝗮 𝗵𝗮𝘀 𝘀𝗼 𝗯𝗮𝗱 𝘁𝗵𝗮𝘁 𝘁𝗵𝗲𝘆 𝗰𝗮𝗻 𝗧𝗔𝗦𝗧𝗘 𝗜𝗧!

Everything you need to know about Joe Biden’s crypto and digital dollar executive order – Euro News

By

Euronews and Reuters • Updated: 09/03/2022

US president Joe Biden signed an executive order on Wednesday requiring the government to assess the risks and benefits of creating a central bank digital dollar, as well as other cryptocurrency issues, the White House said….

Biden’s order will require the US Treasury Department, the Commerce Department, and other key agencies to prepare reports on “the future of money” and the role cryptocurrencies will play.

Biden is planning a new digital currency. | The Hill

But there is an even more important part of the

EO: President

Biden has instructed the federal government and Federal Reserve to lay the groundwork for a potential new U.S.

currency, a

digital dollar.

Biden announces new Digital Currency… EU Times

President Biden admitted recently that the coming ‘New World Order‘ will soon force a digital currency on everybody which will completely replace the traditional U.S. dollar.

On March 9, the Biden administration released an executive order (EO) instructing a long list of federal agencies to study digital assets and to report back to him about their use and proposals to regulate them.

Much of the executive order is focused on cryptocurrencies such as bitcoin and ethereum, which run on blockchain technology.

But there is an even more sinister aspect of the EO that has been completely ignored by the mainstream media: President Biden has instructed the federal government and Federal Reserve to lay the groundwork for a new U.S. currency, a digital dollar that can be tracked and controlled by the government...

Remember during the Obama years there was a 2 TRILLION DOLLAR UNDERGROUND ECONOMY the Cabal could not track REGULATE OR TAX!

So yes there is an E.O just as General Flynn said.

….

Accidental Banking System Failure? Don’t You Believe It.

By Gregory Mannarino TradersChoice.net

The overnight collapse of SVB, (Silicon Valley Bank), has certainly got everyone’s attention, but is this really any surprise at all?

Absolutely not.

The collapse of SVB is just a symptom of the current worldwide economic freefall being deliberately fostered by central banks.

If you are at all familiar with any of my work or have paid attention to the many articles I have written for the Trends Journal, then you are already keenly aware that right now today

the entire financial system is breaking down… and this is NOT any accident. (We are in the early stages of a deliberate systemic failure).

Today the world economy is in an accelerating freefall, teetering on a knifes edge, being deliberately pushed off the financial cliff by central banks who are collectively attempting to crush the existing system only to issue in a new one.

Roughly 8 months ago, I began to warn those who follow my work on YouTube, (check out my older videos), that the banks are in trouble. It just became too obvious, and the current situation with the banks comes down to just THREE things:

no deposits, no loans, and no deals.

In truth, it’s NOT the banks who are in trouble, but as always-We the People. Just some of the fallout from the SVB collapse is this; depositors with more than the government $250K FDIC insurance will never be made whole, and nor will the shareholders, who were just up until a few days ago being told that everything with the bank was sound. Not to mention the throngs of people who just became unemployed. The greatest threat? The collapse of smaller/regional banks will allow the MEGA banks to consolidate power….

𝗜 𝘀𝘁𝗿𝗼𝗻𝗴𝗹𝘆 𝗿𝗲𝗰𝗼𝗺𝗺𝗲𝗻𝗱 𝘆𝗼𝘂 𝗿𝗲𝗮𝗱 𝘁𝗵𝗲 𝗿𝗲𝘀𝘁 𝗼𝗳 𝘁𝗵𝗶𝘀 𝗮𝗿𝘁𝗶𝗰𝗹𝗲.

….

Looking at some comments from yesterday:

para59r Reply to phoenixrising

March 11, 2023 10:06 … #1064592

Just a thought… not sure if it’s right. Inflation comes about when too much money is chasing too few goods. Fed is currently fighting inflation by raising rates. Everyone is screaming about it. Would this be a back door way of eliminating excess money in the market? The ones currently getting whacked are mostly those with lots of excess cash.

The FED was scheduled to raise rates higher on the 22nd of this month and they have been saying they should of raised rates higher than they did (only .5%) when they last met so this one is expected to at minimum be .75% or maybe a full 1%.

Will be interesting to see where they go next. If they do another .5% would that may be another indicator that this bank failure has been manufactured?

Interesting to see the FED is going to meet out of schedule on Monday.

para59r

March 11, 2023 22:13

#1064946

Up to date talk to include banking situation. His message, don’t fall for it.

Yeah it is a Alex Jones interview but he does mostly shut up.

go from 7 minutes.. (20 minute video)

He covers the WHO taking over health care, nuclear war and then the bank collapse.

@ 15 minutes WAIT on withdrawing funds. The way we BEAT the Cabal is to EXPOSE THEM…

@ 17 minutes their are alreadycorporations and elements of the US government BETA TESTING CENTRAL BANK DIGITAL CURRENCY…

….

What Flynn is saying makes sense.

- Bite-me has signed E.O for transition to digital currency.

- This bank failure, which several people say SHOULD NEVER HAVE HAPPENED, is meant to stampede normies into bank runs.

- Bank runs will be used as an excuse to usher in Digital currency.

I am not really fond of listening to Flynn he is a horrible speaker but this fits the facts.

𝗚𝗲𝗻𝗲𝗿𝗮𝗹 𝗙𝗹𝘆𝗻𝗻 𝗶𝘀 𝘀𝗮𝘆𝗶𝗻𝗴 𝘁𝗵𝗲 𝗚𝗹𝗼𝗯𝗮𝗹𝗶𝘀𝘁𝘀 𝗮𝗿𝗲 𝘁𝗿𝘆𝗶𝗻𝗴 𝘁𝗼 𝗦𝗧𝗔𝗠𝗣𝗘𝗗𝗘 𝗔𝗺𝗲𝗿𝗶𝗰𝗮𝗻𝘀 𝗶𝗻𝘁𝗼 𝗯𝗮𝗻𝗸 𝗿𝘂𝗻𝘀 𝘀𝗼 𝘁𝗵𝗲𝘆 𝗰𝗮𝗻 𝘁𝗵𝗲𝗻 𝗵𝗮𝘃𝗲 𝘁𝗵𝗲 𝗲𝘅𝗰𝘂𝘀𝗲 𝘁𝗼 𝘀𝘄𝗶𝘁𝗰𝗵 𝘂𝘀 𝘁𝗼 𝗗𝗜𝗚𝗜𝗧𝗔𝗟 𝗖𝗨𝗥𝗥𝗘𝗡𝗖𝗬!

….

March 12, 2023 13:50

#1065247

@ 45 minutes the guys DROP A BOMB!

On November 7, 2016, Louise Mensch published this article “EXCLUSIVE: FBI ‘Granted FISA Warrant’ Covering Trump Camp’s Ties To Russia” in Heat Street,

“Two separate sources with links to the counter-intelligence community have confirmed to Heat Street that the FBI sought, and was granted, a FISA court warrant in October, giving counter-intelligence permission to examine the activities of ‘U.S. persons’ in Donald Trump’s campaign with ties to Russia.

Contrary to earlier reporting in the New York Times, which cited FBI sources as saying that the agency did not believe that the private server in Donald Trump’s Trump Tower which was connected to a Russian bank had any nefarious purpose, the FBI’s counter-intelligence arm, sources say, re-drew an earlier FISA court request around possible financial and banking offenses related to the server. The first request, which, sources say, named Trump, was denied back in June, but the second was drawn more narrowly and was granted in October after evidence was presented of a server, possibly related to the Trump

campaign, and its alleged links to the two banks; SVB Bank and Russia’s Alfa Bank. While the Times story speaks of metadata, sources suggest that a FISA warrant was granted to look at the full content of emails and other related documents that may concern US persons.” — Heat Street

They refer to this: Jan 19 2023 Bank of America Customers Report “Disappeared” Money From Accounts

Some Bank of America customers said money is missing from their accounts, including funds from Zelle deposits and transactions.

Rey Garcia has trusted Bank of America with his money for 20 years.

…

“I was surprised, like, whoa,” Garcia said. “So I checked my transactions. I had, like, 15 different Zelle transactions. That was, like, a red flag for me right there because I don’t remember doing all that in one day.”

He says almost $700 went missing from his account. He called customer service with no luck getting a representative.

There’s a Bank of America issue where zelle transfers after 1/9 arent being reflected in the balances of ur bank account. I almost lost my mind when I saw $2,000 was missing from my account. Not accepting calls because of “extenuating circumstances” is insane. CALL ME!!!

…Zelle, a peer-to-peer payment processor that is available through more than 1,700 financial institutions, said that the “issue was not the result of any issues with the Zelle Network.”

“We understand that a Zelle Network financial institution may have experienced issues processing some of their customers’ Zelle transactions, which has now been resolved,” a Zelle spokesperson told FOX Business.

#1065256

Banks Ranked by Derivatives

Rank .. Derivatives ………… Bank Name

1 .. $55,387,209,000,000 .. JPMorgan Chase Bank

2 .. $51,794,949,000,000 .. Goldman Sachs Bank USA

3 .. $46,562,329,000,000 .. Citibank

4 .. $22,087,831,000,000 .. Bank of America

5 .. $12,191,517,000,000 ..Wells Fargo Bank

WELLS FARGO...

Mar 10, 2023

Wells Fargo Says “Technical Issue” Causing Customers to See Missing Deposits in Their Accounts

Wells Fargo on Friday scrambled to respond to customers who reported deposits were missing from their accounts.

Customers complained about missing deposits in their accounts.

Many customers were unable to pay bills or buy groceries.

.

.

Another customer complained about a direct deposit disappearing.

One customer complained about being overdrawn because of missing direct deposits.

Wells Fargo responded: “I understand your concern. If you see incorrect balances or missing transaction, this may be due to a technical issue. We apologize for the inconvenience. Your accounts continue to be secure. We are working quickly on a resolution. -Amanda

Another thing about Wells Fargo.

In that AZ hearing, Remember in the testimony Jacqueline Breger mentionedWELLS FARGO!

Hunter’s Burn Notice: Miami & Houston Edition

…Additionally, Wells Fargo is right next to

Greenberg Traurig LLP, like in one’s backyard. Greenberg was tied to the stock warrants and a blind trust of 22.5% that goes through Continental.

Wells Fargo

was Hunter and Jim Biden’s Bank of choice from the Laptop from Hell….

Failed Silicon Valley Bank Funded Democrats, Establishment RepublicansSVB’s PAC had some eye-opening expenditures.

…FEC filings from 2020 and 2022 show the Silicon Valley Bank PAC, the Super PAC associated with the failed bank, donated in

2020 and

2022 to Political committees directly aligned with Congressional Democrats and pro-impeachment Trump Republicans.

On December 22nd, 2020, well after the 2020 election, Silicon Valley Bank PAC donated to Citizens for Waters, a political committee aligned with Congress Woman Maxine Waters(D-CA). On the same date, Silicon Valley Bank Pac donated to Friends of Gregory Meeks, a political committee aligned with Congressman Gregory Meeks (D-NY). Anthony Gonzales for Congress also received a donation from Silicon Valley Bank Pac on December 22nd, 2020. Anthony Gonzales was among the few Republican Congressmembers to vote to impeach Trump following January 6th….

Interestingly the only political committee Silicon Valley Pac gave to during the 2022 cycle was to friends of Mark Warner. Mark Warner won reelection in 2020 and is not up again until 2026.

Congressional records show that Silicon Valley’s Bank lobbyist in 2022 where the Franklin Square Group, LLC. Franklin Square Group was founded by Josh Ackil, who worked for then-President Bill Clinton. Ackil openly brags about his workings with the Clintons on his Franklin Square Group profile and in media outlets such as the Hill….

Tweet from:

Bill Ackman

The gov’t has about 48 hours to fix a-soon-to-be-irreversible mistake.

By allowing @SVB_Financial to fail without protecting all depositors, the world has woken up to what an uninsured deposit is — an unsecured illiquid claim on a failed bank.

Absent

or

acquiring SVB before the open on Monday, a prospect I believe to be unlikely,

or the gov’t guaranteeing all of SVB’s deposits, the giant sucking sound you will hear will be the withdrawal of substantially all uninsured deposits from all but the ‘systemically important banks’ (SIBs). These funds will be transferred to the SIBs, US Treasury (UST) money market funds and short-term UST. There is already pressure to transfer cash to short-term UST and UST money market accounts due to the substantially higher yields available on risk-free UST vs. bank deposits.

These withdrawals will drain liquidity from community, regional and other banks and begin the destruction of these important institutions. The increased demand for short-term UST will drive short rates lower complicating the

@federalreserve ’s efforts to raise rates to slow the economy.

Already thousands of the fastest growing, most innovative venture-backed companies in the U.S. will begin to fail to make payroll next week. Had the gov’t stepped in on Friday to guarantee SVB’s deposits (in exchange for penny warrants which would have wiped out the substantial majority of its equity value) this could have been avoided and SVB’s 40-year franchise value could have been preserved and transferred to a new owner in exchange for an equity injection. We would have been open to participating.

This approach would have minimized the risk of any gov’t losses, and created the potential for substantial profits from the rescue. Instead, I think it is now unlikely any buyer will emerge to acquire the failed bank. The gov’t’s approach has guaranteed that more risk will be concentrated in the SIBs at the expense of other banks, which itself creates more systemic risk.

For those who make the case that depositors be damned as it would create moral hazard to save them, consider the feasibility of a world where each depositor must do their own credit assessment of the bank they choose to bank with. I am a pretty sophisticated financial analyst and I find most banks to be a black box despite the 1,000s of pages of

@SECGov filings available on each bank.

SVB’s senior management made a basic mistake. They invested short-term deposits in longer-term, fixed-rate assets. Thereafter short-term rates went up and a bank run ensued. Senior management screwed up and they should lose their jobs.

The

@FDICgov and OCC also screwed up. It is their job to monitor our banking system for risk and SVB should have been high on their watch list with more than $200B of assets and $170B of deposits from business borrowers in effectively the same industry.

The FDIC’s and OCC’s failure to do their jobs should not be allowed to cause the destruction of 1,000s of our nation’s highest potential and highest growth businesses (and the resulting losses of 10s of 1,000s of jobs for some of our most talented younger generation) while also permanently impairing our community and regional banks’ access to low-cost deposits. This administration is particularly opposed to concentrations of power. Ironically, its approach to SVB’s failure guarantees duopolistic banking risk concentration in a handful of SIBs. My back-of-the envelope review of SVB’s balance sheet suggests that even in a liquidation, depositors should eventually get back about 98% of their deposits, but eventually is too long when you have payroll to meet next week. So even without assigning any franchise value to SVB, the cost of a gov’t guarantee of SVB deposits would be minimal. On the other hand, the unintended consequences of the gov’t’s failure to guarantee SVB deposits are vast and profound and need to be considered and addressed before Monday. Otherwise, watch out below.

This guy sounds like he knows what he is talking about.

Start at 12 minutes go to around 20 minutes.

Prior to this “TruReporting” mentioned the bank loans were to SOLAR AND WIND. Those are the companies they are talking about. Loans went out no money came back in . (Do not forget all the Biden $$$ for green energy) He seems to thing it might have been a money laundering scam.

He also talks about how it is similar to the 2008 Lehman Brothers scam under Obama.

….

They are mentioning that the companies effected are going to go to Biden for BAILOUTS!

GEE, and Biden JUST HAPPENS TO WANT TO INCREASE THE DEBT CEILING– IMAGINE THAT! (Snarl)

As Wolfie always says

AND LOGIC…

RDS (@guest_1065398)

Online

March 12, 2023 18:18

#1065398

IMO, this guy may have a point —

https://markcrispinmiller.substack.com/p/with-big-banks-cbdcs?utm_source=substack&utm_medium=email

2 hours ago

“With big banks going under, CBDC’s can’t be far behind—and if we don’t STOP them, “lockdown” will be total, and eternal, for us all”

Yours Truly: If one is reading the article correctly, Mr. Miller is of the opinion that since “vaccination” isn’t “working out”, and that the truth is being shown about Jan6, the “Next Big Thing” that will be “deployed” is economic collapse and the imposition of Central Bank Digital Currencies.

RDS (@guest_1065398)

Online

March 12, 2023 18:18

IMO, this guy may have a point —

https://markcrispinmiller.substack.com/p/with-big-banks-cbdcs?utm_source=substack&utm_medium=email

2 hours ago

“With big banks going under, CBDC’s can’t be far behind—and if we don’t STOP them, “lockdown” will be total, and eternal, for us all”

Yours Truly: If one is reading the article correctly, Mr. Miller is of the opinion that since “vaccination” isn’t “working out”, and that the truth is being shown about Jan6, the “Next Big Thing” that will be “deployed” is economic collapse and the imposition of Central Bank Digital Currencies.

I assume that Circle is this company.

https://www.circle.com/en/

Best I can tell they have 9 Billion in assets.

Partnered with Mellon, Black Rock and lessors.

In short.

Circle is a global financial technology firm that’s at the center of digital currency innovation and open financial infrastructure. We bridge the traditional financial system and the world’s leading public blockchains to unlock growth for businesses and investors around the world.

I wonder if they were one of companies that got early warning to pull out?

There is the crypto thing, again.

Crypto is cited in every financial institution going under, recently.

^^^ NOT a coincidence, in my shallow way of thinking. Never trust crypto.

https://media.patriots.win/post/LxstkheNeqDE.jpeg

https://media.patriots.win/post/q2lrDWCiHBFA.png

Arnaud Bertrand – Twitter – Charts at link.

What a chart in the FT: China is now as big as the US and the EU **COMBINED** (!) in terms of manufacturing value added (a measure of the net-output of all manufacturing activity in a country).

Just 15 years ago it was smaller than either one of these 2. Crazy fast change! &

And the craziest part is that its share of world manufacturing increases like this despite shrinking as a share of China’s GDP

In other words, other constituents of China’s GDP (like services) grow even faster than manufacturing. &

And the proportional growth isn’t finished, as the EU’s share is bound to decrease *a lot*

https://s.w.org/images/core/emoji/14.0.0/svg/1f53d.svg, which will increase other countries’ proportionally (and probably China’s disproportionally, since it is the best positioned to capture more manufacturing).

𝗕𝗥𝗘𝗔𝗞𝗜𝗡𝗚: 𝗙𝗲𝗱, 𝗙𝗗𝗜𝗖 𝗗𝗶𝘀𝗰𝘂𝘀𝘀𝗶𝗻𝗴 𝗕𝗮𝗰𝗸𝘀𝘁𝗼𝗽 𝘁𝗼 𝗠𝗮𝗸𝗲 𝗦𝗩𝗕 𝗗𝗲𝗽𝗼𝘀𝗶𝘁𝗼𝗿𝘀 𝗪𝗵𝗼𝗹𝗲 𝗮𝗻𝗱 𝗦𝘁𝗲𝗺 𝗖𝗼𝗻𝘁𝗮𝗴𝗶𝗼𝗻 𝗙𝗲𝗮𝗿𝘀 – 𝗖𝗡𝗕𝗖

3 hr ago

[QUOTE]

The government and their useful idiot secretary of treasury Janet Yellen have just done an about face and are now telegraphing that they will be intervening yet again in “free” markets.

It’s a publicly traded crime scene.… The media wants to make it a crypto story, but it’s not. This is a worldwide money laundering story through these two networks with a crypto wrapper.

—

So why would an illegitimate Federal government, its criminal agencies and the private central banksters at the Fed provide the optics of yet another (quasi) bailout of a bank that failed due in no small part to the very conditions that these central planners caused with their unhinged policies in the first place?

Bailing out SVB will be a drop in the bucket fiat-wise compared to the orgy of money printing that went down during the scamdemic.

Between banks and centralized crypto corporations simultaneously failing, the narrative options for collapse are more than sufficient.

There are many other banks like SVB that are in long-duration securities and have irresponsible and dangerous exposure to treasuries and other bonds. Short sellers started circling these institutions weeks ago, and more will pile in betting against these insolvent banks.

Here is how this may end up playing out:

- The bailout is a headfake

- When other banks start failing over the coming weeks the government apparatchiks like Yellen will claim that they did their best by backstopping SVB while the systemic contagion worsens all around

- By bailing out SVB they are providing the requisite narrative to cover their asses when their masters pull plug on the entire global financial system

- SBV may be used as the “Black Swan” excuse for their PSYOP-MARKET-CRASH, and they can once again claim that they did their utmost (e.g. “The banking system is contained” a la Ben Bernanke’s “Subprime is contained”), but in the end oops sorry the cascading bankruptcies and bank runs were too much for the government to handle

- Pain and fear from frozen bank accounts, food insecurity, inflation, etc. is the perfect means of herding people into the social credit score system of CBDC’s, UBI, never-ending DEATHVAX™ boosters, climate lockdowns, 15 minute cities, etc. & etc.

This is all by design.

Meanwhile, depositors have already begun to panic:

.

.

[UNQUOTE]

kalbokalbs(@kalbokalbs)

Offline

Coyote

Reply to RDS

March 12, 2023 19:41

Still listening to one of the video’s. Corbett. Lots a nuggets.

CBDC – A digitl concentration Camp.

CBDC – When the government TRIES to INSTALL CBDC, I expect:

- 100% CALL TO A GENERAL STRIKE – Shut The Country Down.

- Americans of ALL types will say, FUCK NO.

- ALL 50 States, 50 State Capitals, large cities, small cities…

- Rich, poor, across all blue collar, white collar, retired…

- Gotta believe there will be Widespread, Massive, HELL NO To CBDC.

YES, Coviciocy / Covidiot Injections are being exposed / failing. The J6 narrative LIES are being exposed.

CBDCs will be, ARE a bridge to far. Vast Majority of Americans WILL rise up against CBDC, once they learn, CBDC – Are A Digital Concentration Camp.

Or so I believe.

phoenixrising(@phoenixrising)

Offline

Wolverine

March 12, 2023 21:01

Okay, I guess I skipped over zerohedge’s piece on the Fed’s Statement … that was a mistake!

lookie here:

“The Fed also said that it is prepared to address any liquidity pressures that may arise, which in turn has just unveiled the first bailout acronym of the new crisis: the Bank Term Funding Program, or BTFP. Some more details:

The financing will be made available through the creation of a new Bank Term Funding Program (BTFP), offering loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral. These assets will be valued at par.

The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell those securities in times of stress.

The Fed explains that the Department of the Treasury will make available “up to $25 billion from the Exchange Stabilization Fund as a backstop for the BTFP.” And while the Federal Reserve – which was completely clueless about this banking crisis until Thursday – does not anticipate that it will be necessary to draw on these backstop funds, we anticipate that the final number of needed backstop liquidity be somewhere north of $2 trillion.

What is more notable is that the BTFP – or Buy The Fucking Pivot – facility, will pledge collateral at par, not at market value, thus giving banks credit for all those hundreds of billions in unrealized net losses, and allowing banks to “unlock liquidity” based on losses which the Fed and TSY now backstop!

full article here https://www.zerohedge.com/markets/svb-latest-developments-live-blog-fdic-auction-failed-svb-assets-underway

Brave and Free (@guest_1065461)

Offline

March 12, 2023 20:38

Depositors won’t lose any $$

https://www.federalreserve.gov/newsevents/pressreleases/monetary20230312b.htm

No $$ lost except

Shareholders and certain unsecured debtholders will not be protected. Senior management has also been removed. Any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks, as required by law.

Coothie

It’s still short of The Iceland Plan if former management is still walking around….

Management gets bonuses AND an opportunity to buy SVB stock, BELOW market.

phoenixrising

pennies on the $ — JP Morgan and Jamie Daimon just got richer!

https://www.zerohedge.com/markets/bitcoin-bullion-surge-after-fed-bailout-rate-hike-odds-plummet

US Financial Regulators shut down Signature Bank

https://www.cnbc.com/2023/03/12/regulators-close-new-yorks-signature-bank-citing-systemic-risk.html

click link for statement in image form https://t.me/intelslava/45751

Fed just bailed out SVB depositors while Yellen is saying there’s no bailouts. There it is.

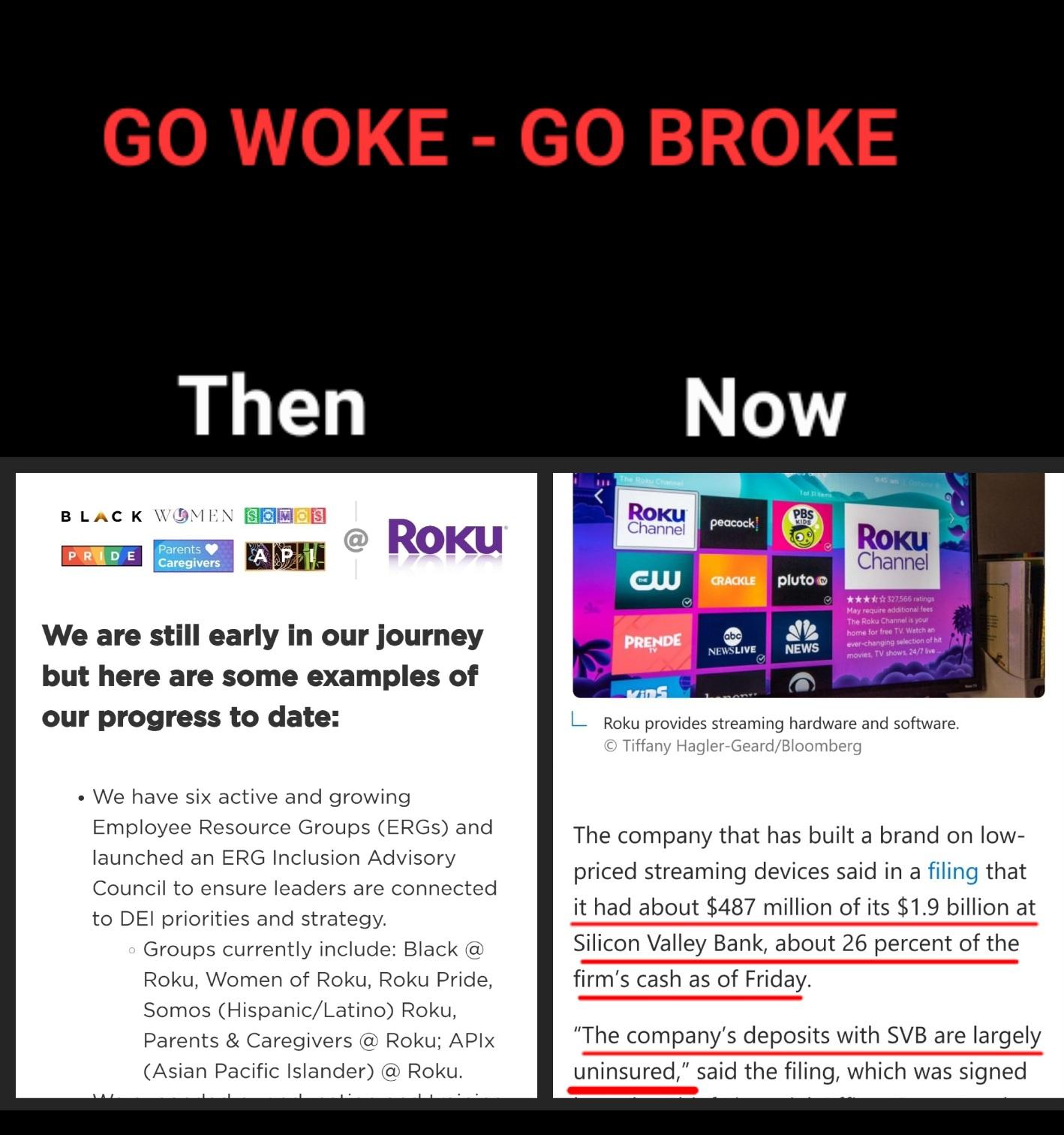

““These banks are badly run because everybody is focused on diversity and all of the woke issues and not concentrating on the one thing they should, which is shareholder returns,” ~ Home Depot Founder https://www.zerohedge.com/political/home-depot-founder-tells-americans-wake-after-silicon-valley-bank-collapse

{kind=link}

{kind=link}

{kind=link}